Fix and Flip Loan Guide: Everything Real Estate Investors Need to Know

In the early stages of launching your rental investment strategy and looking to make some serious cash in the real estate game? Well, look no further than fix and flip loans — a go-to financing option for both the novice and the experienced real estate investor. Why waste time with traditional mortgages when you can dive headfirst into the world of flip and bridge financing?

When is a fix and flip loan the best financing solution for a rental investment property?

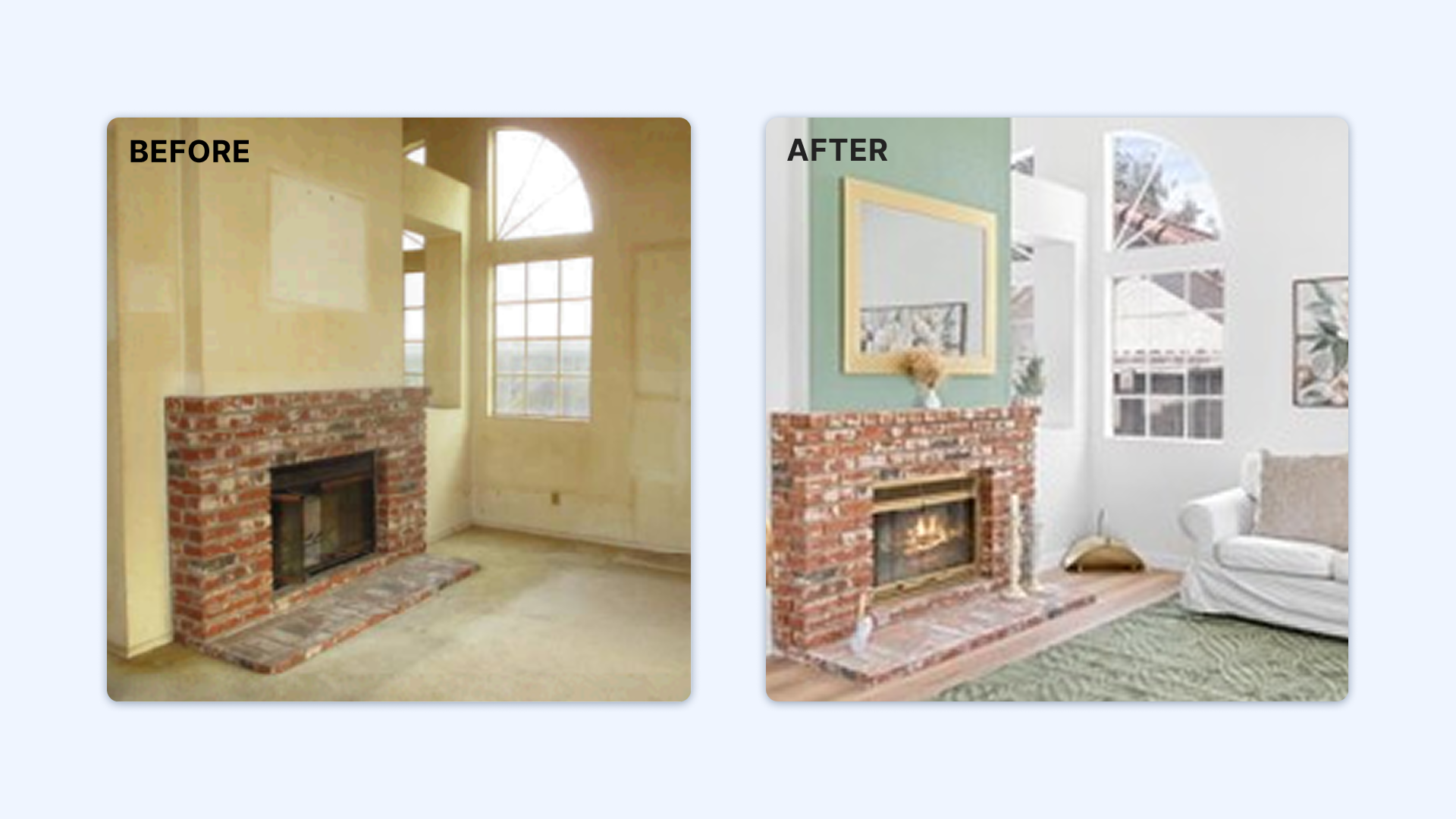

Fix and flip loans are tailor-made for those looking to snatch up properties that need a little TLC. With these short-term loans, you can quickly purchase your dream fixer-upper and get down to business. Whether it’s a trust deed or an appraisal, we’ve got all the documentation covered.

But here’s the best part: fix and flip loans not only cover the purchase price but also fund those much-needed renovations. So, you can turn that run-down house into a stunning home without breaking the bank and without multiple loan solutions.

Ready to dive into this exciting world of property flipping? Let’s get started!

Note: This article will walk you through everything you need to know about fix and flip loans, from finding the perfect property to securing funding in no time.

Understanding Fix and Flip Loan Programs

Various loan programs are available to cater to different needs in the fix and flip industry. These programs offer financing options that can help investors purchase properties, renovate them, and then sell them for a profit. There are a few key points to understand.

- Loan options: There are several loan programs tailored specifically for fix and flip projects. Some common options include:

- Hard money loans: These short-term loans can sometimes carry higher interest rates, but they provide quick funding.

- Rehab loans: Designed for properties that require significant renovations, these loans cover both the purchase price and renovation costs.

- Bridge loans: Ideal for investors who need temporary financing until they secure long-term funding.

- Interest rates and terms: The interest rates and terms of fix and flip loans vary depending on the lender’s requirements and the borrower’s qualifications. Generally, interest rates for these types of loans tend to be higher than traditional mortgages due to their short-term nature.

- Loan-to-value (LTV) ratios: Lenders determine the amount of financing available based on the property’s loan-to-value ratio (LTV). This ratio represents the percentage of the property’s value that can be borrowed. Typically, fix and flip lenders offer LTV ratios ranging from 70% to 90%. CoreVest will allow up to 90%.

- After Repair Value (ARV): Lenders will also estimate and consider the ARV of a property before determining how much financing to extend on a single fix and flip project. The ARV is the estimated future worth of a property after all planned renovations, repairs, and upgrades are completed.

- Business plan and experience: To qualify for a fix and flip loan, borrowers must demonstrate a solid business plan outlining their strategy for purchasing, renovating, and selling properties. Lenders like CoreVest consider investors’ experience in real estate investing when assessing their eligibility.

Here’s a sample Fix and Flip loan scenario:

- If the purchase price is $500K

- And the renovation budget is $75K

- The total project cost would be an estimated $575K

- Assuming the loan applicant or borrower qualifies for 90% of the purchase price, and at 75% of After Repair Value or ARV:

- The initial loan at closing would equal $450K (90% of Purchase Price)

- The renovation loan would be $50K (100% Renovation Budget)

- And the total loan amount would be $525K

- Here, the ARV would need to be estimated at $700k (since total loan is $525K or 75% of ARV) for the borrower to achieve 90%.

- If the ARV comes back lower than $700K, the borrower will be required to bring that difference in to closing.

Best Options for Fix and Flip Loans

Traditional banks may not be the best choice. Several other options are available that provide more flexibility and convenience for borrowers.

Private lenders offer an alternative to traditional banks. While they may have higher interest rates, they often provide more flexible terms. Some private lenders even specialize in fix and flip loans, making them well-suited for this type of investment.

Another option to consider is hard money lenders. Some of these lenders specifically focus on providing loans for fix and flip projects. One advantage of working with hard money lenders is their faster approval times compared to traditional banks.

For those seeking a convenient way to access multiple loan options, online lending platforms can be a great resource. These platforms allow borrowers to compare different loan offers from various lenders in one place, saving time and effort.

To summarize the best options for fix and flip loans:

- Traditional banks: Strict requirements but may offer competitive rates.

- Private lenders: More flexible terms, fast approval times, and competitive rates.

- Hard money lenders: Often specialized in fix and flip loans with faster approval times but sometimes higher rates.

- Online lending platforms: Provide convenient access to multiple loan options from different lenders, allowing you to shop around.

By exploring these alternatives, investors can find the best fit for their fix and flip projects without being limited by the constraints of traditional banking institutions. CoreVest is a private lender with a vast product portfolio that includes similar products to what a hard money lender could offer, but typically at lower rates.

How Fix and Flip Loans Work

Investors looking to purchase a property for the purpose of fixing it up and selling it, commonly known as “fix and flip,” often rely on fix and flip loans to finance their projects. These loans are specifically designed to provide funding for the purchase and renovation of properties with the intention of selling them quickly for a profit.

When applying for a fix and flip loan, investors typically submit their application before acquiring the property. Lenders assess various factors, such as the investor’s experience and creditworthiness, as well as the potential value of the property after renovations are completed.

Once approved, funding is usually provided in stages throughout the project. This allows investors to access funds as they progress with their renovations. The staged disbursement ensures that there is enough capital available to cover expenses at each phase of the project. CoreVest, however, offers flexibility here. CoreVest can provide the funding through multiple stages, or as one large draw for renovation funds at the end of the project.

Repayment options for fix and flip loans primarily involve two methods: selling the renovated property or refinancing into a long-term mortgage. Investors typically aim to sell the property quickly after completing renovations to repay the loan in full.

If market conditions are not favorable for an immediate sale, investors may choose to refinance into a long-term mortgage and hold the property, allowing them more time to sell while making regular mortgage payments. They can refi into something longer term if they plan to hold as a rental.

Alternatively, if they just need more time to sell, they can either exercise an extension (typically 3 to 6 months) or do a new 12-month refinance. If the goal is to eventually sell, lenders will often see the extension of 12-month refi option as a better fit given alternative; and more long-term products can sometimes come with prepayment penalties.

Exploring Hard Money Loans for Fix and Flip Projects

Hard money loans offer a valuable financing option for real estate investors looking to undertake fix and flip projects. Unlike traditional loans, hard money loans are asset-based, meaning they rely on the property itself as collateral rather than credit history. Let’s delve into the key aspects of hard money loans that make them an attractive choice for investors in the fix and flip market.

- Approval based on property value: When seeking a hard money loan, real estate investors don’t have to worry about personal financials. Instead, approval is primarily based on the value of the property being purchased or renovated. This allows individuals with less-than-ideal credit scores or limited financial history to secure funding for their projects.

- Higher interest rates: It’s important to note that hard money loans typically come with higher interest rates compared to traditional mortgages. This is because hard money lenders assume a greater risk by providing funds quickly and without scrutinizing personal finances extensively. The higher interest rates compensate for lenders taking on more risk.

- Quick funding advantage: One significant advantage of hard money loans is their ability to provide quick funding. Traditional loan processes can be lengthy and time-consuming, potentially causing investors to miss out on lucrative opportunities in the competitive real estate market. With hard money loans, investors can secure properties before other buyers through expedited approval and funding processes.

By exploring hard money loans as an option for fix and flip projects, real estate investors gain access to flexible financing solutions that prioritize property value over personal financials. These asset-based loans allow individuals with varying credit histories to pursue their investment goals confidently while taking advantage of quick funding opportunities in today’s dynamic real estate market.

Financing Options Beyond Traditional Fix and Flip Loans:

Fix and flip loans are not the only choice available. Depending on individual circumstances and preferences, there are several alternative avenues to explore.

- Personal Savings or Funds from Family/Friends: Many investors choose to tap into their personal savings or seek financial assistance from family members or friends. This option allows them to access funds without involving external lenders or incurring interest charges.

- Crowdfunding Platforms: Another popular option is utilizing crowdfunding platforms that connect investors with potential projects. These platforms allow multiple individuals to contribute smaller amounts towards funding a project, providing a diverse pool of loan funds.

- Line of Credit or Home Equity Loans: If an investor already owns a primary residence, they may consider leveraging their existing assets through a line of credit or home equity loan. This approach enables them to utilize the equity built in their property as collateral for financing their real estate investment ventures.

- Partnerships and Resource Pooling: Real estate investors often collaborate with like-minded individuals by forming partnerships or joint ventures. By pooling resources, such as capital, skills, and expertise, partners can collectively finance projects while sharing the associated risks and profits.

Conclusion

Fix and flip loans offer several benefits for real estate investors looking to renovate and sell properties quickly. These specialized loan programs provide the necessary financing to purchase distressed properties, fund renovations, and cover holding costs until the property is sold.

One of the key advantages of fix and flip loans is their flexibility. Unlike traditional mortgage loans, fix and flip loans are designed specifically for short-term investment projects. They have faster approval processes, allowing investors to secure funding quickly and take advantage of time-sensitive opportunities in the market.

Fix and flip loans often have more lenient eligibility requirements compared to traditional loans. This means that even if you have a less-than-perfect credit score or limited experience in real estate investing, you can still potentially access the funds needed to pursue your fix and flip projects.

Another benefit is that these loans typically provide higher loan-to-value ratios compared to other types of financing options. This allows investors to leverage their capital more effectively by borrowing a larger portion of the purchase price and renovation costs.

To maximize your success with fix and flip loans, it’s important to explore different options available in the market. Consider working with reputable hard money lenders who specialize in providing financing for fix and flip projects. Be aware that there are alternative financing options beyond fix and flip loans that may better suit your specific needs.

In summary, fix and flip loans offer real estate investors a convenient way to finance their renovation projects. By understanding how these loan programs work and exploring various options available, you can make informed decisions that align with your investment goals.

Fix and Flip FAQs

Yes! Fix and flip loans are known for their flexible eligibility requirements. Even if you have bad credit, you can still qualify for these specialized loan programs as long as you meet other criteria such as having a solid business plan or demonstrating previous successful flips.

Approval times for fix and flip loans are typically faster than traditional mortgage loans. Depending on the lender, you can receive approval within a matter of days or weeks, allowing you to move forward with your investment project swiftly.

No, fix and flip loans cater to both experienced investors and those new to real estate investing. While some lenders may prefer borrowers with a track record of successful flips, there are loan programs available specifically designed for beginners or investors with limited experience.

Fix and flip loans usually have short-term loan terms ranging from six months to two years. The specific duration will depend on factors such as the scope of renovations and the projected timeline for selling the property.

Yes, fix and flip loans can be used to finance properties purchased at auctions. However, it’s important to note that each lender may have different requirements regarding auction purchases, so it’s advisable to discuss this with potential lenders beforehand.

Most fix and flip loans require collateral in the form of the property being financed. The property serves as security in case of default on the loan payments.

Some lenders may impose prepayment penalties if you pay off your fix and flip loan before the agreed-upon term ends. It’s crucial to review the terms of your loan agreement carefully to understand any potential penalties or fees associated with early repayment. Some loan options don’t have any prepayment penalties. And some lenders will disguise the prepayment as a “minimum interest requirement”, meaning they have to earn X amount of dollars in interest, or else you will be charged. CoreVest does not have either prepayment penalties or minimum interest requirements on their fix and flip loan.